Меф гашиш шишки бошки купить

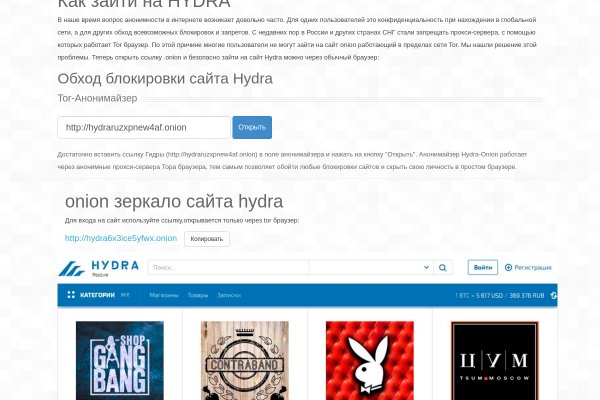

Вскоре представитель «Гидры» добавил подробностей: «Работа ресурса будет восстановлена, несмотря ни на что. Официальные зеркала kraken Выбирайте любое kraken зеркало. Отметим и то, что, используя зеркало, вы можете произвести обнал криптовалют, купить бошки закладками, а также найти другие цифровые товары. Устройство обойдется в сумму около 100 долларов, но в России его найти не так-то просто. Также не лишним будет упомянуть о системе оплаты на Kraken. Валторны Марк Ревин, Николай Кислов. Информация включает в себя: адрес расположения сервера, используемое программное где обеспечение и другую информацию. Подпишись что бы быть в курсе. Чтобы войти на сайт Блэкспрут. Onion - Lelantos секурный и платный email сервис с поддержкой SMTorP tt3j2x4k5ycaa5zt. Пожелаем им удачи, а сами займёмся более благодарным делом. Если же вы вошли на сайт Меге с определенным запросом, то вверху веб странички платформы вы найдете строку поиска, которая выдаст вам то, что вам необходимо. Также сразу после входа он получит возможность внести деньги на баланс личного кабинета, чтобы тут же приступить к покупкам. Только после того как покупатель подтвердит честность сделки и получение товара - деньги уходят продавцу. Специально для новых пользователей площадки mega darknet market существует скидочный купон «fsdufhig позволяющий получить скидку 20 на второй заказ, активировать его можно в личном кабинете, либо в момент совершения сделки. Площадка мега Маркет ценит активных юзеров и всячески награждает их приятными бонусами. Ребёнок в этом сложном процессе вряд ли разберётся. На нашем представлена различная информация о, ссылки собранная из открытых источников, которая может быть полезна при анализе и исследовании. Вам не нужно переживать и волноваться, если по каким-то причинам вы не смогли подключиться к сайту сразу. Мега Дарк нет это темная сторона интернета, позволяющая пользователям приобретать товар в анонимном режиме.

Меф гашиш шишки бошки купить - Купить наркоту

Все сделки на темном рынке заключаются с использованием криптовалюты, что позволяет дополнительно защитить клиента от нежелательного внимания силовых ведомств. Ну, любой заказ понятно, что обозначает. ( зеркала и аналоги The Hidden Wiki) Сайты со списками ссылок Tor ( зеркала и аналоги The Hidden Wiki) torlinkbgs6aabns. Чтобы выполнить обмен, выберите интересующее вас направление, например банковская карта BTC, кликните на сайт и укажите необходимую вам сумму. isbn.Предыдущая страница: omg официальный сайтСледующая страница: ссылка на гидру зеркалоКомментарии (Всего 9 комментариев 1) в 05:49 opaqag: Я не знаю, каким оружием будет вестись третья мировая война, но четвёртая палками и камнями.(2) в 03:54 grafabblaccon: Добрый вечер. Для того что попасть в Даркнет вам всего лишь надо скачать Tor браузер. Возможность оплаты через биткоин или терминал. Употребление соли вызывает очень стойкую зависимость, поэтому самому избавиться от нее сложно. Kraken darknet market активно развивающаяся площадка, где любой желающий может купить документы, ПАВ, банковские карты, обналичить криптовалюту и многое другое. Гобой София Гришина. Перейти на форум Рутор форум Главный форум черного рынка Представляем вашему вниманию форум даркнета под названием Rutor. Спутниковое телевидение, оборудование для приема и декодирования. Переверните человека на бок, если он дышит расстегните воротник, чтобы было легче дышать. Все города РФ и СНГ открываются перед вами как. Неважно, Qiwi перевод или оплата через Bitcoin, любой из предложенных способов полностью анонимный не вызывающий подозрения к вашей личности. Вся ответственность за сохранность ваших денег лежит только на вас. Бесправным членом ( извиняюсь за каламбур) что-то не хочется быть на такой площадке. Администраторы постоянно развивают проект и вводят новые функции, одними из самых полезных являются "автогарант" и "моментальные покупки". Является зеркалом сайта fo в скрытой сети, проверен временем и bitcoin-сообществом. Хочу заметить что сайты имеющие вот такие имена rrdgrtsdfdertreterwetro2hsxfogfq. Здесь пользователи находили себе друзей по интересам и формировали постоянные сообщества. Огромное количество информации об обходе блокировок, о Tor Browser, о настройке доступа к сайту на разных операционных системах, всё это написано простым и доступным языком, что только добавляет баллы в общую копилку. В итоге купил что хотел, я доволен. Дарк нет площадка это онлайн сообщество, которое существует для обмена информацией между людьми, пользующимися анонимным и неорганизованным доступом к интернету. Подключится к которому можно только через специальный браузер Tor. После успешной регистрации система предложит вам выбрать город, который будет установлен по умолчанию, это облегчит процесс покупки в последующие разы. Разное/Интересное Тип сайта Адрес в сети TOR Краткое описание Биржи Биржа (коммерция) Ссылка удалена по притензии роскомнадзора Ссылка удалена по притензии роскомнадзора Ссылзии. Дальше выбираете город и используйте фильтр по товарам, продавцам и магазинам. Репутация При совершении сделки, тем не менее, могут возникать спорные ситуации. Отсутствие аппетита Следы от инъекций Симптомы передозировки героином Симптомы передозировки проявляются сразу после инъекции: Начинают синеть губы и ногти Спутанное сознание Бледнеет коероина. Список антивирусов Если злоумышленникам удастся проникнуть в компьютер пользователя любыми способами, то он будет пытаться извлечь для себя важную информацию.

При разовом употреблении следы наркотика находятся в человеке 48 часов. Закладки делают обычные люди, которыми движет желание заработать. При этом все надписи зашифрованы, ни в интернете, ни на объявлениях, которые встречаются на улице, вы не встретите прямой фразы: «Ищем продавца наркотиков». Как выглядит героин и где его купить. Синтетический наркотик соль популярен как у новичков, так и у наркоманов со стажем. Кстати факт вашего захода в Tor виден провайдеру. isbn.Предыдущая страница: omg официальный сайтСледующая страница: ссылка на гидру зеркалоКомментарии (Всего 9 комментариев 1) в 05:49 opaqag: Я не знаю, каким оружием будет вестись третья мировая война, но четвёртая палками и камнями.(2) в 03:54 grafabblaccon: Добрый вечер. Есть цена которую приходится платить за мнимый кайф. Каким образом попасть на сайт в Darknet. Если рот заполнен рвотной массой, освободите его. Официальные зеркала kraken Выбирайте любое kraken зеркало. Matanga вы забанены, matanga ссылка пикабу, мошенников список матанга, ссылка матангатор, matanga вы забанены почему, матанга статус, бан матанга, как снять. Рутор даркнет Цитата Несколько месяцев подряд интересуетесь закрытым сообществом darknet? 1566868 Tor поисковик, поиск в сети Tor, как найти нужный. Мега наркота и ее передвижения не должны быть отслежены правоохранителями, поэтому на сайте используются 3 самые популярные криптовалюты: BTC XMR usdt Если на вашем кошельке не хватает крипты, вы можете совершить обмен с qiwi прямо на сайте Мега. Браузер Tor в Google Play Когда браузер будет установлен, для выхода в теневую сеть нужен будет список специальных ссылок на русские сайты. Onion-сайтов. Настройка Tor Browser для посещения. Напишите нам и мы поможем вам решить вашу проблему или подскажем как пройти регистрацию на Rutor. Р как в России, так и на Западе. Показываю как открыть сайты, заблокированныe РосКомНадзором без VPN. Также можете задать критерии фильтрации, например, тип закладки и варианты доставки товара. Употребление героина приводит к сильному привыканию, а ломка после чрезвычайно болезненна и мучительна. Подросток губит свое здоровье, перспективы и шанс на счастливую и беззаботную жизнь. Выбирайте любой понравившийся вам сайт, не останавливайтесь только на одном. Эти преимущества делают площадку привлекательным выбором для людей, ищущих анонимный и удобный доступ к интернету. Имейте в виду, что необходимо выполнить вход и настроить VPN для доступа к площадке. Всем привет, в этой статье я расскажу вам о проекте ТОП уровня defi, у которого. Ответ на этот вопрос полюбоваться на продавцов в магазине Мега Дарк нет Маркет. Сеть. У нас опубликована всегда рабочая блэкспрут ссылка. После выполнения операции деньги поступят на ваш счет, обычно это занимает до 30 минут или по наличию двух подтверждений сети. Спасибо! Располагается в темной части интернета, в сети Tor. Список ссылок на самые популярные сайты Даркнета. Onelonhoourmypmh.onion/signup) безопасный и безвредный сайт, позиционируется как социальная сеть; Социальная сеть Onelon Facebook (https www.